Bruce Brammall, 19 September, 2018, Eureka Report

SUMMARY: SMSFs pull ahead on performance, as trustees adjust to rule changes to play the game smarter, with better advice.

Active investment and contribution decisions by DIY trustees in recent years are leading to outperformance and better tax outcomes.

Self-managed superannuation funds have embraced the new deductible super contributions rules, more than doubling quarterly contributions in FY2018.

And a significant move out of cash and into equities has lifted SMSF investment performance above MySuper investment options in recent years.

New surveys show trustees made some significant strategic changes last financial year.

SMSF administrator SuperConcepts says contributions to super have lifted from around $3498 a quarter in June 2017 to $8623 in June 2018 across the 2600 funds they look after.

SuperConcepts said the increase was a direct result of the changes to contributions rules on 1 July 2017.

On that date, the “10% rule” was removed, allowing employees to make direct, deductible, contributions to their funds for the first time. Previously, employees had to make these contributions via salary sacrifice through their employer. But employers were not legally obliged to offer salary sacrifice.

The 10% rule had previously effectively restricted anyone who earned more than 10% of their income as an employee from making concessional contributions to super by means other than via their employer.

The removal of the 10% rule “was a positive rule change that SMSF trusteees have embraced with gusto because it was only ever available to the self-employed,” SuperConcepts executive manager Phil LaGreca said.

Over the same period, benefit payments have more than halved, as SMSF pensioners look to preserve their pension in the wake of other rule changes.

SuperConcepts said its average super fund dropped income payments from $50,313 to $22,289, in reaction to the new $1.6 million Transfer Balance Cap (TBC).

This was the result of pensioners learning to manage the drawdowns from their pension funds.

But because higher income levels were still required by many clients, these clients tended to opt to take lump sum payments to top up their income.

These can now be taken from their accumulation accounts when they have met a condition of release. And many older pensioners had rolled back portions of their pensions to accumulation where they exceeded a pension account of $1.6m.

The second option is to make partial commutations from their pensions to help manage their Transfer Balance Account (TBA).

A TBC is the limit (currently $1.6m, but this will rise over time). A TBA is the actual amount that you have used of your TBC. Pensioners can reduce their TBA by making partial commutations of the pensions back to accumulation, from where they can make a lump sum payment.

“This again reflects the significant impact of the legislative changes that applied from 1 July 2017 where the capital value of pension accounts is limited to $1.6 million which resulted in a lower level of pension payments being required to be paid,” LaGreca said.

The move to “lump sum” payments for income increased throughout the yearm, according to SuperConcepts’ data. It started the year as around 10% of outflows to members, to 90% pension payments, but ended the year at 21% lump sum and 79% pension payments.

The good news is that super fund trustees are adjusting to the new rules well and are, according to LaGreca, getting professional advice on how to do this properly.

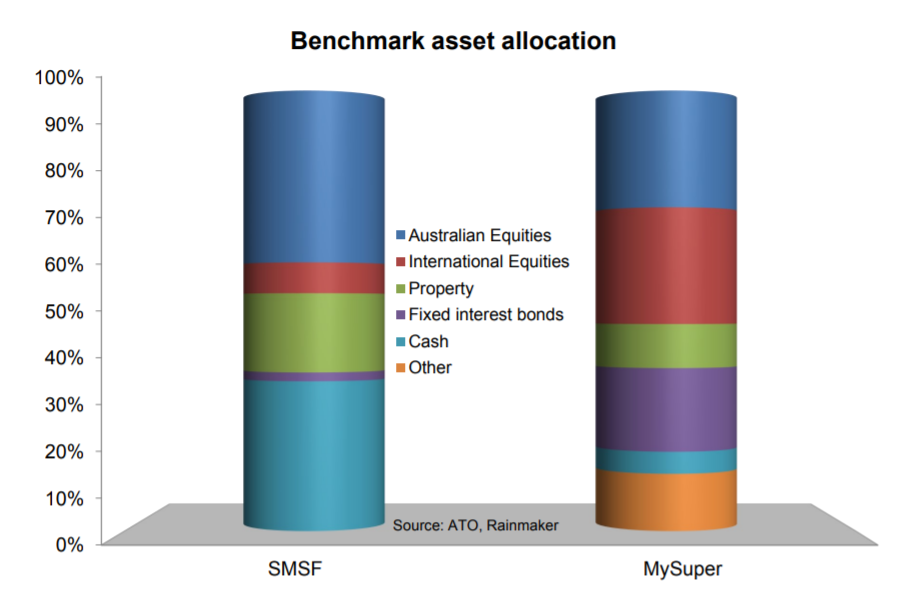

Another survey, by SuperGuard 360, shows that SMSF’s asset allocation has delivered superior returns in recent times also.

SuperGuard 360’s survey compares a basket of the default MySuper funds to the actual asset allocation of SMSFs, as put out by the ATO in its quarterly statistics.

The SMSF Reference Index returned 10.5% for the year to the end of July 2018, versus 10.2% for the Default Index (MySuper).

SMSFs are also marginally ahead over three years – 7% versus 6.8%.

But over five years, the Default Index is ahead by a significant 0.9% – 8.4% versus 7.3%.

Graph 1: Asset allocation of SMSF v MySuper

Source: SuperGuard 360 SMSF Performance Indices

The difference in performance over various periods comes down to the above graph. As has long been noted, Australian SMSFs just seem to be more comfortable with Australian shares, property and cash. And they hold massive amounts of those assets, while being underweight in international shares, fixed interest and “other”.

*****

The information contained in this column should be treated as general advice only. It has not taken anyone’s specific circumstances into account. If you are considering a strategy such as those mentioned here, you are strongly advised to consult your adviser/s, as some of the strategies used in these columns are extremely complex and require high-level technical compliance.

Bruce Brammall is managing director of Bruce Brammall Financial and is both a licensed financial adviser and mortgage broker. E: bruce@brucebrammallfinancial.com.au . Bruce’s sixth book, Mortgages Made Easy, is available now.